Your company designs and builds great products. For each product sold, you’re making a margin. In a market with growing competition and vocal customers, that margin is under pressure and tempering EBIT growth. At the same time, you hear about healthy margins on services. To satisfy your CFO and shareholders you want to tap into this service lifecycle margin contribution. Consequently, we see OEM organizations turning their attention to service revenue growth. And when they do, what personas will drive the revenue growth agenda?

To help answer that question, here’s a story: About 15 years ago I met a salesperson at an event rejoicing ‘the day of sales and after-sales’. With conviction I explained the value of after-sales services. He was very resolute: “If there is so much margin in selling services and we crave bonuses, why aren’t we jumping on the service bandwagon?” Less than two weeks later another salesperson shook my belief in service value by saying “Profitability, who cares? Certainly not sales.”

These two experiences have humbled me toward the revenue growth agenda. True, service may have a more favorable margin contribution than product sales. Still, you first need to make the initial product sale before you can sell after-market services. Hence, the revenue growth agenda is not an either product or service play, but a joint effort.

To quantify the EBIT/margin contribution potential of a joint revenue play, we’ve developed the mind-the-gap exercise. What if you have visibility of all units sold? What if all product owners have a commercial service lifecycle relationship with you? What if all those service contracts are of type ‘gold’? Compare this maximum, this total addressable market (TAM) with your current service revenue. Either you ‘claim’ this gap…or somebody else will.

Playing a different tune

As simple as it sounds, knowing the gap is existential. As a company you’ll have to make an informed decision where you want to generate margin contribution, how you want to fuel EBIT and deliver on shareholder expectation. What portion of the lifecycle margin contribution do you ‘claim’ as OEM, grant to the indirect sales channel or to our competitors?

The underlying paradigm of service lifecycle revenue is that customers buy products to use them, to derive value from its output/outcome. This drives asset owners to mitigate product-downtime, and, as products become more complex, they will rely on service organizations who can guarantee uptime. This is where the OEM, as designer of the product and owner of the intellectual property, must make a business model choice: do we sell-and-forget or do we sell-and-service? And once that decision is made, multiple personas come into play to underpin revenue growth:

- Engineering

- Sales

- Service/After-Market

Engineering

It makes a big difference if you design a new product for a sell-and-forget model versus sell-and-service. In the former, you optimize the design for manufacturing and focus on the margin contribution from the product sales (capex). Any after-market revenue is incidental, non-recurring and non-predictable. The installation, maintenance and operating manual are packaged in the product sale as mandatory deliverable, not as intellectual property you can monetize.

In a sell-and-service model you optimize product design for serviceability and operability. Since you have a vested revenue interest in supporting the product throughout its entire lifecycle (opex), you’ll make deliberate decisions on how and who can sustain the product.

- Do we repair on component or module level?

- Is this a self-service activity or does it require trained/ certified resources?

- Can we fix this fault code via remote, onsite or depot-service?

- Is firmware embedded, open-source or firewalled?

- Do we design for retrofitting and upgrades?

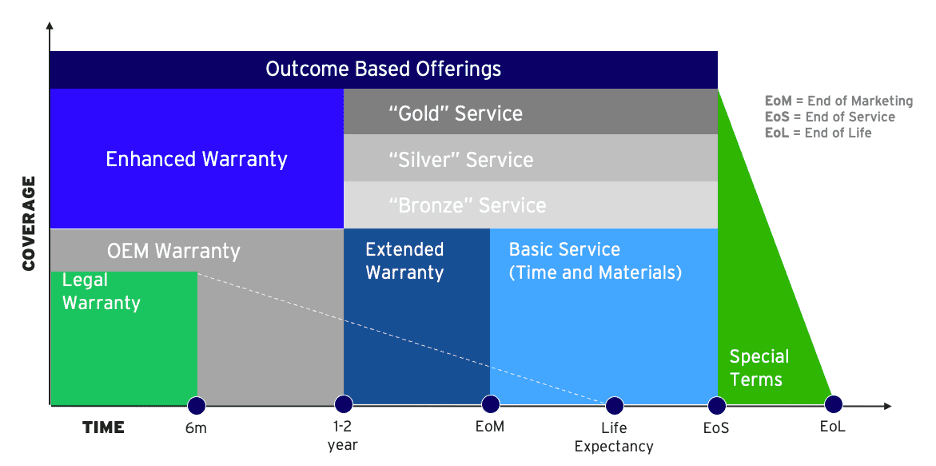

Ultimately, one can plot all those service design decisions in a lifecycle chart. Each node represents a touchpoint, an activity, an effort, a cost and a revenue. This engineering plan-view is the basis for revenue generation/margin contribution in sales and service.

Sales

In a sell-and-forget model, sales may choose not to complicate the sale by talking about lifecycle opex. As a result, after-market revenue and margin contribution are unpredictable.

In a sell-and-service model, sales have a choice to generate revenue/margin contribution through a mix of capex and opex. The more engineering embraces design-for-service, the larger the lifecycle services portfolio, the more sales opportunities.

The engineering-lifecycle-view is both a great tool to educate prospects on what to expect during the operational lifecycle, as well as an instrument for cross and upselling. Once the prospect ‘acknowledges’ the lifecycle chart, it becomes a matter of visiting the nodes and ask: “will you do it yourself or shall I do it for you?”

Thirdly, this engineering-lifecycle-view is a pivotal building block in reshaping the relationship between OEM and distributors/resellers. Once you can visualize and quantify the revenue potential of after-market, OEM and reseller can renegotiate the dealership agreement, sharing profit and partnering in joint service delivery, upholding product quality and brand perception.

Service/After-Market

Once products are in the field, actual product behavior can be measured. Because each customer use is different, service delivery personas need (near) real-time tools to detect deltas between plan and actual.

Without such tools, you’ll probably deliver free service. According to Aberdeen State of Service this amounts up to 14% of your service cost. Call it leakage or missed revenue.

Without comparing plan versus actual on installed product level, you may miss out on the customer context and upsell potential. For example, when my car goes for maintenance, the mechanic can tell me if I drove my car according to engineering specifications or if my actual wear-and-tear is different. It may come as no surprise that informed and empowered technicians are the best salesmen, advising me to replace components, suggest an upgrade, or buy a new product.

Team play

Based on the above, we can ascertain that service revenue growth is not owned by a single persona, but it is a team play. The team can use the mind-the-gap exercise to quantify the revenue potential. Once that potential is defined, your CFO and shareholders will certainly task one of those personas to drive the EBIT contribution.

Published on PTC Blog.